New SIFMA Analysis: The Fed & CCAR 2020 – Stay the Course for the Sake of Economic Recovery

- Coryann Stefansson

Key Points

- There is no evidence that the COVID-19 experience requires revisions to the CCAR 2020 GMS factor shocks. In fact, in most asset classes, the GMS factor shocks are multiples of the COVID-19 one-day and 10-day most adverse experience. Many asset classes are near or within reach of early March levels.

- Layering on an extreme tail scenario for capital market products on top of the already conservative 2020 CCAR framework will result in an unjustified increase in the SCB. An unnecessary higher SCB will negatively impact the capacity of banks to support economic recovery including providing credit and liquidity to households and businesses, contributing to orderly markets, and intermediating the capital markets.

- The CCAR approach essentially double taxes capital markets participants and capital market products. It estimates post stress capital under the severely adverse scenario (the nine-quarter path) reflecting two loss estimation paths: the Global Market Shock and Large Counterparty Default instantaneous losses and the trading losses based on the macroeconomic scenario.

Layering In An Additional Extreme Tail Scenario in CCAR 2020 Could Impede the U.S. Economic Recovery

Comprehensive Capital Analysis and Review (CCAR) results are expected to be announced within the next month. As noted in our recent blog, we remain concerned the Federal Reserve (the Fed) will incorporate additional and more extreme stress projections for capital markets products and participants that were not part of the CCAR 2020 exercise. This is particularly disturbing because CCAR 2020 will be used to size the initial Stress Capital Buffer (SCB), which was finalized earlier this year. Layering in an extreme tail scenario on top of the already severe 2020 CCAR framework may result in an unjustified increase in the SCB, particularly when economic recovery is reliant on banks to provide credit and liquidity to households and businesses, contribute to orderly markets, and support financial intermediation in the capital markets.

SIFMA has repeatedly expressed concern regarding the CCAR approach to capital market products and those firm’s which are active participants. SIFMA has commented on the overly conservative assumptions related to the Global Market Shock (GMS) and the Large Counterparty Default (LCD) elements of CCAR. These components are only applied to a subset of CCAR filers which are comprised of the most active capital market participants including those with considerable processing and custodial operations.

SIFMA believes CCAR 2020 GMS is already overly severe and in combination with the additional CCAR treatment of trading book exposures maintain more than ample capital for trading book and large counterparty exposures.

CCAR Treatment of Capital Markets Products and Participants Is Sufficiently Severe

The GMS and the LCD are components of the Fed’s annual point-in-time capital assessment, known as CCAR. The CCAR process is applicable to the largest U.S. bank holding companies (BHCs) and U.S. intermediate holding companies of foreign banking organizations (IHCs) [1]. The GMS and the LCD components are only applied to a subsection of CCAR banks. The GMS component is mandatory for those firms which meet the Fed’s criteria[2] for significant trading activity[3]. These firms are also subject to the LCD, however, the LCD component is also applicable to banking organizations which the Fed considers having significant processing and custodian operations[4].

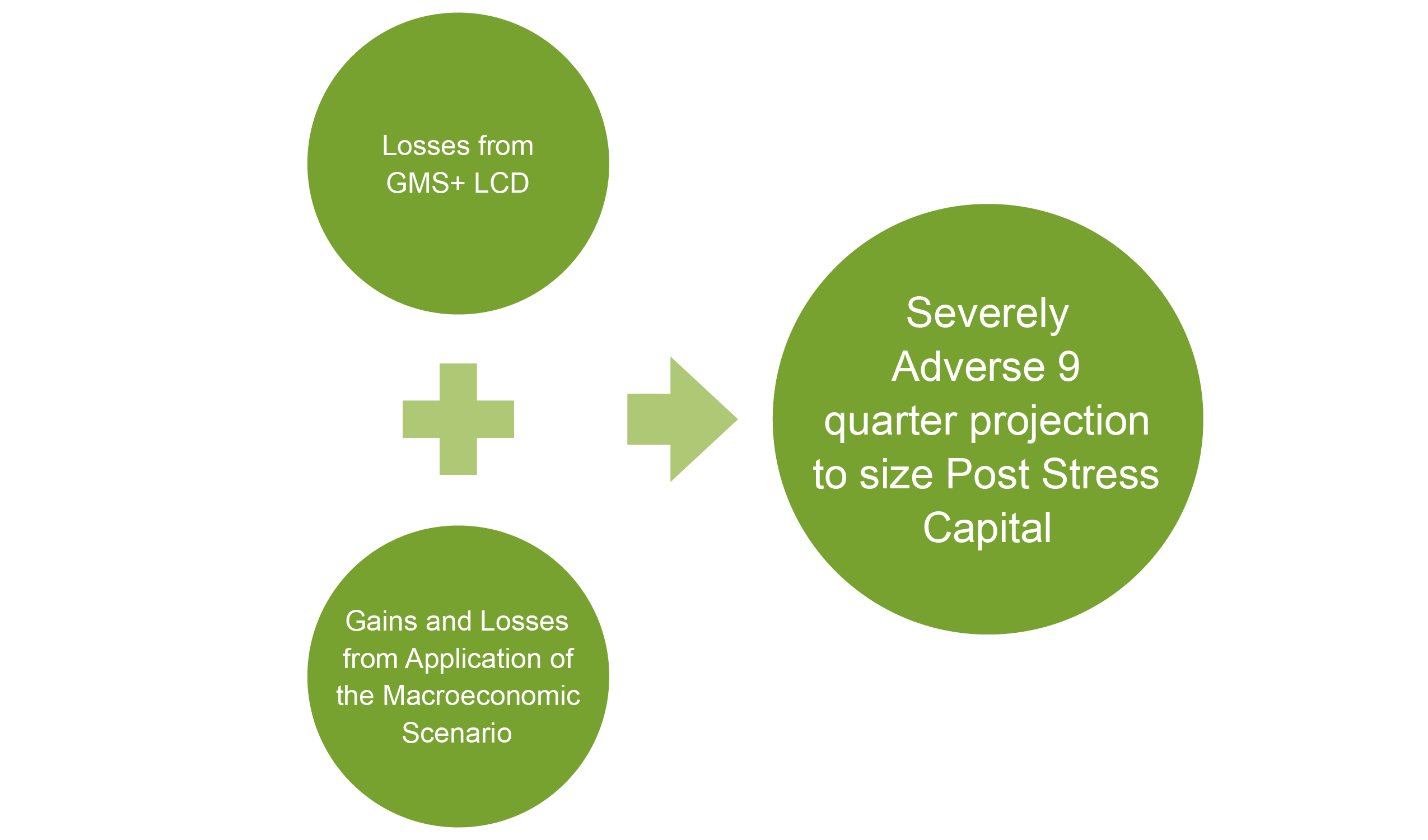

CCAR requires Capital Market Participants to generate losses from the application of the GMS and the LCD and from the application of the macroeconomic scenario to the trading book under the severely adverse scenario to estimate losses.

CCAR requires Capital Market Participants to generate losses from the application of the GMS and the LCD and from the application of the macroeconomic scenario to the trading book under the severely adverse scenario to estimate losses.

The GMS component is designed to estimate losses from an instantaneous shock to a BHC/IHC’s trading and private equity positions and counterparty exposures. GMS generated losses are estimated by applying a series of pricing and market data points called the GMS factor shocks that are provided annually by the Fed. The CCAR process also requires the firm to separately estimate losses from the trading book and counterparties through the application of the severely adverse macroeconomic scenario that is part of the broader CCAR stress test. As a reminder, the severely adverse macroeconomic scenario is driven by economic and market indicators provided by the Fed and are realized over a nine-quarter forward looking path. The severely adverse scenario is applied to all of a firm’s positions including the trading book. To estimate post-stress capital, a firm must reflect losses that are generated by the severely adverse scenario’s impact on the trading book plus the losses from the GMS instantaneous shock.

Similar to the GMS component of CCAR, firms subject to the LCD are required to estimate losses and related impacts on capital from the unexpected and instantaneous default of their largest counterparty. The LCD requires a firm to select the largest counterparty by determining which counterparty, after the application of the GMS factor shocks produce the largest losses. Like the GMS, the LCD component is an add-on, meaning the losses produced by this test are added to the losses that are driven by the application of the macroeconomic scenarios in the severely adverse scenario which already includes losses associated with a series of counterparty defaults.

SIFMA has long advocated that the application of the GMS and LCD components and the severely adverse macroeconomic scenario to trading book and counterparty exposures to generate losses essentially double taxes capital markets participants and products.

The CCAR 2020 GMS Factor Shocks Are Severe and the COVID-19 Experience Does Not Warrant Additional Shocks

The rigor of the 2020 GMS factor shock is well illustrated by a series of visual depictions of GMS factor shocks for a limited subset of asset classes over the past seven CCARs. We have also charted the COVID-19 experience along with the 2020 GMS factor shock, the most adverse GMS factor shock and the historical most adverse shock ever over a one-day and 10-day experience to provide perspective on the severity of the COVID-19 experience.

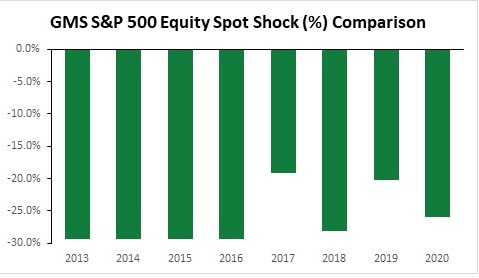

S&P 500 Spot Equity Shock Comparison: The 2020 S&P 500 Spot Equity GMS Factor Shock is Severe

There are a series of U.S. and Foreign equity shocks that are employed in the GMS, one of the factor shocks used for spot equity shock applied to the S&P 500 index.

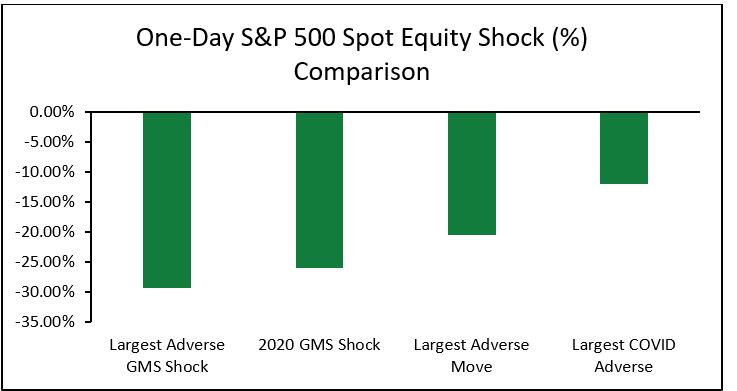

The 2020 S&P 500 Spot Equity GMS Factor Shock is More Severe than the COVID-19 Experience On Both a One-day and 10-day Observation Basis

Using the one-day observation, the single worst day performance of the S&P 500 index during the COVID-19 period was a decline of nearly 12%, as compared to the 2020 GMS factor shock of a 26% drop. In other words, the 2020 GMS factor shock is more than double the decline that was experienced during COVID-19. If we broaden the comparison to the most adverse one-day historical experience in the S&P 500 index ever, the GMS factor shock is still more severe by 30%.

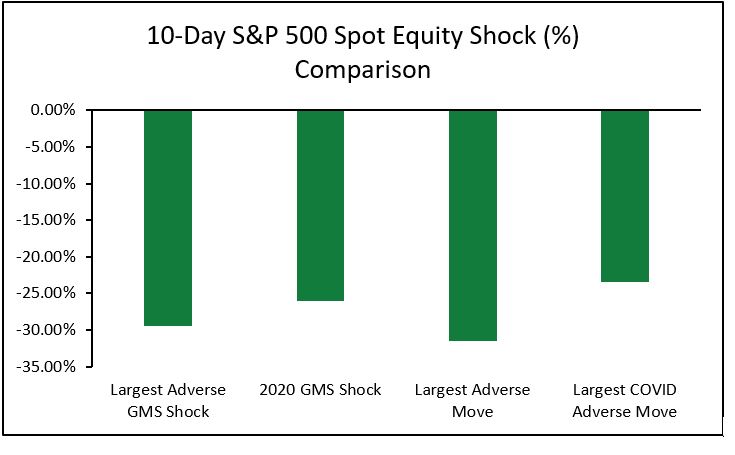

Shifting to the 10-day period, the COVID-19 experience represented a 23% decline in the S&P 500 index which was still less severe that the 2020 GMS S&P 500 spot equity shock. Historically, the most adverse S&P 500 index performance over a 10-day period, exceeds the GMS shock and the COVID-19 experience by 21% and 35% respectively.

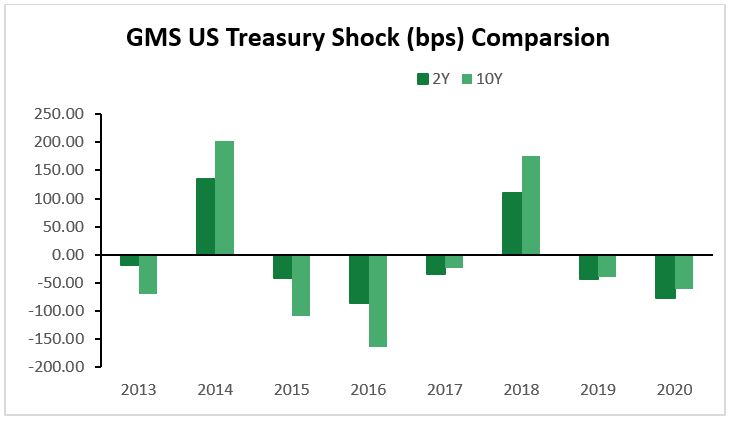

US Treasury Rate Shocks for the 2-year and 10-year Exposures

The GMS employs a series of factor shocks across sovereign and municipal debt of various maturities and geographies. Below compares the GMS factor shock for two-year and 10-year U.S. Treasury spreads across the seven years of CCAR. Additionally, we analyze the COVID 19 experience, the 2020 GMS factor shock and the historical most adverse movements over a one-day and 10-day observation period.

The graph above depicts the series of GMS factor shocks applied to two-year and 10-year treasury exposures over the past seven years. The factor shocks for these asset classes vary significantly year-over-year in terms of direction (spread widening/spread tightening) and severity. Clearly, the 2014 and 2018 GMS factor shocks standout as dramatic shifts year-on-year. The 2020 GMS factor shocks for U.S. Treasury Rates are more severe than 2019 and are more significant for the two- year bond than the 10-year bond. Accordingly, the 2020 US Treasury rate shocks for the two-year and the 10-year are more punitive by 83% and 50%, respectively, than the previous year.

The graph above depicts the series of GMS factor shocks applied to two-year and 10-year treasury exposures over the past seven years. The factor shocks for these asset classes vary significantly year-over-year in terms of direction (spread widening/spread tightening) and severity. Clearly, the 2014 and 2018 GMS factor shocks standout as dramatic shifts year-on-year. The 2020 GMS factor shocks for U.S. Treasury Rates are more severe than 2019 and are more significant for the two- year bond than the 10-year bond. Accordingly, the 2020 US Treasury rate shocks for the two-year and the 10-year are more punitive by 83% and 50%, respectively, than the previous year.

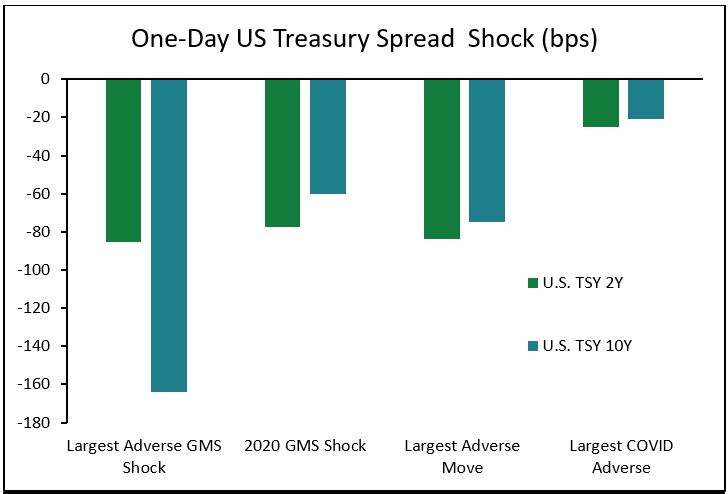

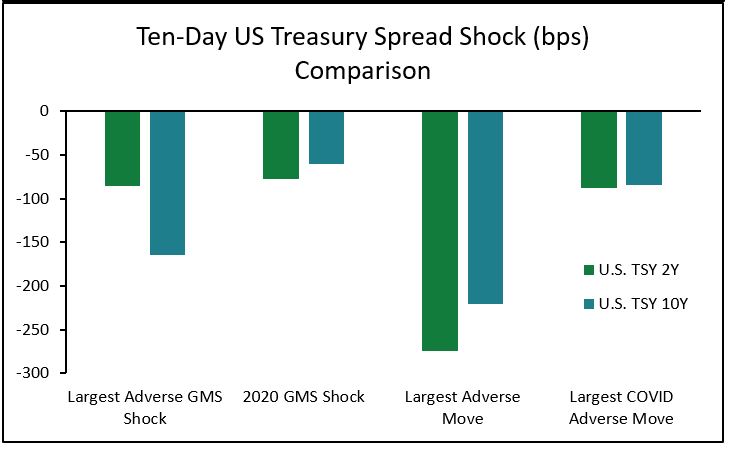

When considering the COVID-19 experience and using a one-day comparison, the 2020 GMS U.S. Treasury factor shock far exceeds the COVID-19 most adverse one-day spread movement for both the two-year and 10-year US treasury spreads. The two-year GMS factor shock is over 200% greater than the COVID-19 one-day move. The 10-year GMS factor shock is 186% greater than the one-day COVID-19 experience. However, using the ten-day observation period, the COVID-19 spread movement for both the two-year and 10-year were greater than the GMS factor shock by approximately 13% and 40%, respectively. This was prompted both by rate cuts and desire for US treasuries during market dislocations.

When comparing the COVID-19 most adverse one-day experience to the most adverse one-day historical move ever in the two-year U.S. Treasury, the COVID-19 experience is 236% lower. Performing the same analysis over the 10-day observation period for the two-year treasury, the COVID-19 experience is 213% lower. Similarly, we found that the COVID-19 experience is 257% lower than the most adverse one-day move in the 10-year U.S. Treasury. Finally, using a 10-day observation period for the 10-year U.S. Treasury, the COVID-19 experience is 163% lower than the most adverse 10-day historical move.

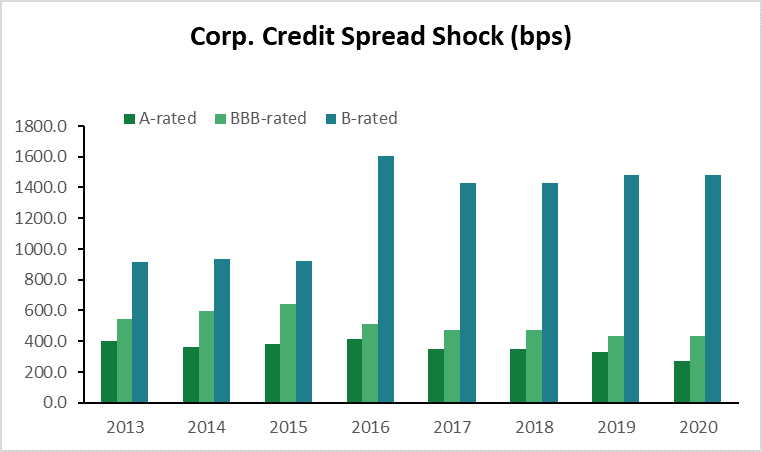

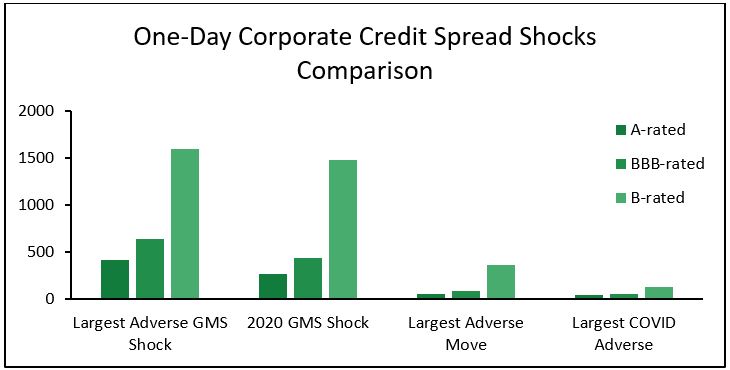

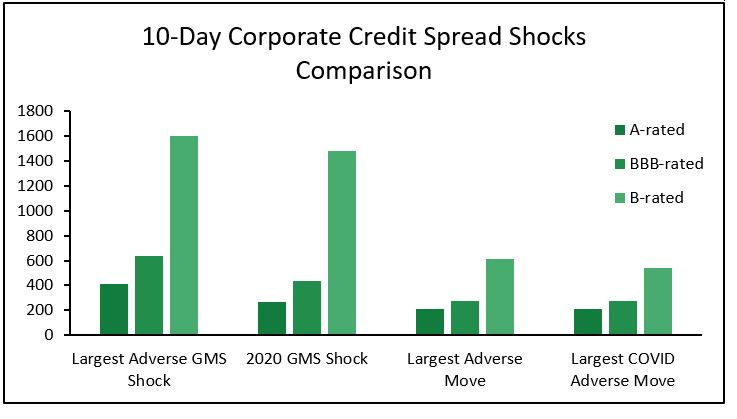

Corporate Credit Shocks Comparison

The GMS aligns a series of different factor shocks to generate losses in Corporate Credit trading exposures. To compare the Corporate Credit GMS factor shocks over time, we selected one of the factor shocks that applies spread shocks by ratings. Below we compare the 2020 GMS factor shock in comparison to the past seven years of CCAR GMS factor shocks. Additionally, we analyzed the COVID-19 experience, the 2020 GMS factor shock, and the historical most adverse movements over a one-day and 10-day observation period.

This chart illustrates how the Fed’s approach to sizing the spread shock has shifted over time. Overall, the GMS shocks applied to A and BBB rated exposures have declined somewhat since the initial years of the GMS (2013-2015). Conversely, the Fed has significantly amplified the shock to B rated exposures (over 60% between the 2013 GMS and the 2020 GMS for B rated exposures) from the initial years of the GMS.

This chart illustrates how the Fed’s approach to sizing the spread shock has shifted over time. Overall, the GMS shocks applied to A and BBB rated exposures have declined somewhat since the initial years of the GMS (2013-2015). Conversely, the Fed has significantly amplified the shock to B rated exposures (over 60% between the 2013 GMS and the 2020 GMS for B rated exposures) from the initial years of the GMS.

The 2020 Corporate Credit factor shocks for BBB and B rated exposures were unchanged from 2019, whereas the factor shock for A rated exposure declined approximately 18% from the prior year. In terms of comparison to the most adverse one-day historical experience, the 2020 factor shock for A rated exposures is almost five times the historical most adverse one-day movement in A rated credit spread. The 2020 GMS factor shock for BBB rated credit spreads is more than five times greater than the historical most adverse one-day movement in BBB rated spreads. Finally, the 2020 GMS factor shock for B rated credit spreads is approximately four times greater than the historical most adverse one-day movement. In fact, for B rated spreads not only has there never been a one-day adverse movement as large as the 2020 GMS factor shock, it is more severe than a six-month series of historical one-day most adverse price moves.

When Considering the COVID-19 Experience, the GMS 2020 Factor Shocks Were Far in Excess for A, BBB and B Rated Corporate Credit Over the One-day and 10-day Observation Periods.

On a one-day basis, the 2020 GMS factor shock for A rated exposure was seven times more severe than the COVID-19 single worse day experience. The 2020 GMS factor shock for BBB rated exposure was more than eight times more severe than the COVID-19 single worse day experience. Finally, the 2020 GMS factor shock for B rated exposures was 12 times more severe that the COVID-19 single worse case experience.

Shifting to 10-day observation, the 2020 GMS factor shock for A rated exposure was 30% greater than the COVID-19 most adverse 10-day period. For BBB rated exposure, the GMS factor shock was 57% more severe than the COVID-19 most adverse 10-day move. Finally, the 2020 GMS factor shock for B rated exposures was 178% -greater than the COVID-19 most adverse 10-day move.

In terms of COVID-19 experience, historical one-day moves were sizeable larger. For example, the most adverse historical moves for one-day for A, BBB and B rated exposure were 39%, 46% and 191% higher, respectively.

Switching to the 10-day observations, the A and BBB rated moves during COVID-19 are now the largest 10-day moves, but importantly are still significantly less than the 2020 GMS factor shock for the same rated exposures. The B rated COVID-19 experience was 14% lower than the most adverse historical experience.

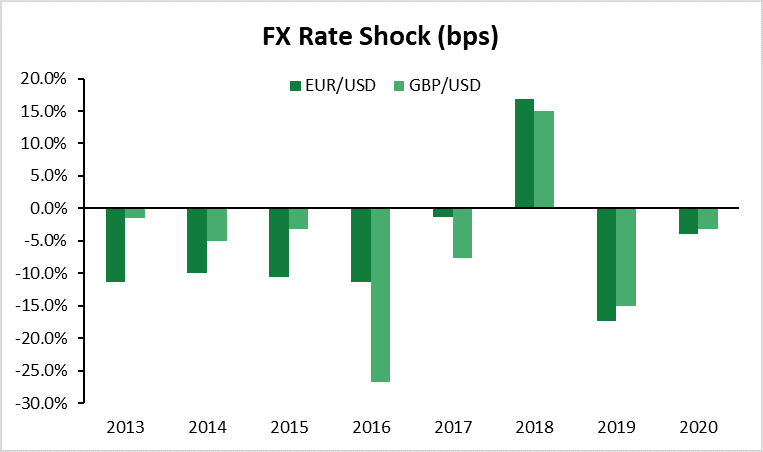

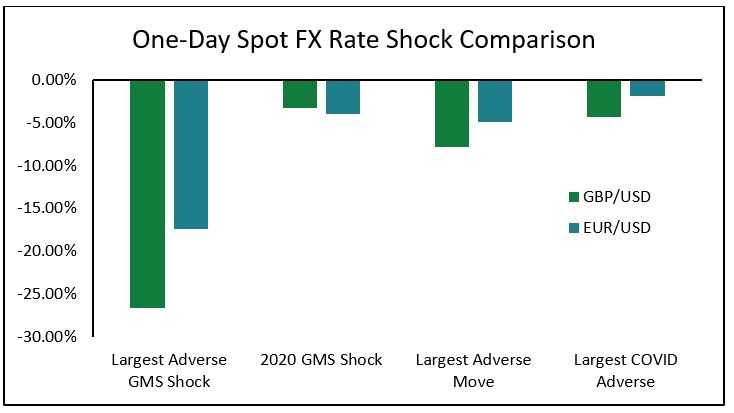

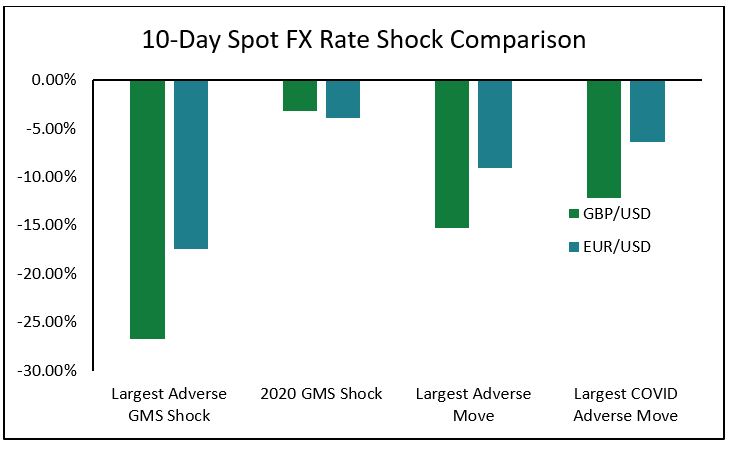

Spot FX Rate Shock

There are several spot and forward FX GMS factor shocks that are applied to currency positions in the trading book. To compare the FX GMS factor shocks over time, we selected the FX spot factor shocks for GBP/USD and EUR/USD. Below compares the 2020 GMS factor shock for both currency pairs in comparison to the past seven years of CCAR GMS factor shocks. Additionally, we analyzed the currency pairs performance in the COVID-19 experience with the 2020 GMS factor shock and the historical most adverse movements over a one-day and 10 -day observation period.

The GMS factor shocks for spot EUR/USD and GBP/USD positions for the past seven CCARs are illustrated in the chart to the left. Both the EUR/USD and the GBP/USD spot factor shocks were substantially less severe in 2020 than in the previous year, however, in 2019, the EUR/USD GMS rate shock was the most severe since the inception of CCAR. The 2019 GBP/USD factor shock was severe however but not nearly as harsh as the 2016 factor shock. The 2020 factor shock for spot EUR/USD represents about 80% of the historical one-day most adverse performance; whereas the 2020 factor shock for spot GBP/USD represents about 41% of the historical one-day most adverse performance.

The GMS factor shocks for spot EUR/USD and GBP/USD positions for the past seven CCARs are illustrated in the chart to the left. Both the EUR/USD and the GBP/USD spot factor shocks were substantially less severe in 2020 than in the previous year, however, in 2019, the EUR/USD GMS rate shock was the most severe since the inception of CCAR. The 2019 GBP/USD factor shock was severe however but not nearly as harsh as the 2016 factor shock. The 2020 factor shock for spot EUR/USD represents about 80% of the historical one-day most adverse performance; whereas the 2020 factor shock for spot GBP/USD represents about 41% of the historical one-day most adverse performance.

As previously mentioned, the 2020 GMS factor shocks for GBP/USD and EUR/USD were considerably less severe than in previous years. During the COVID-19 period the most adverse one-day price move for the GBP/USD exceeded the 2020 GMS factor shock by roughly 33%. Conversely, the most adverse one-day price move for EUR/USD was slightly more than 50% lower than the 2020 GMS Factor Shock. If we shift our comparison of the most adverse one-day period during COVID-19 to the most adverse historical period for the GBP/USD, we find that the one-day COVID-19 experience is 84% less severe. We noted similar results for the EUR/USD, where the most adverse one-day COVID-19 experience was 163% less severe than the most adverse one-day historical move ever.

Analysis expanded to the include the most adverse 10-day rate moves during COVID-19 for both the GBP/USD and EUR/USD finds that the COVID-19 experience exceeded the 2020 GMS factor shock by almost 300% and 64%, respectively. Nevertheless, the COVID-19 experience was considerably less than the most historical adverse move in both the GBP/USD by 26% and the EU/USD by 42%.

Assumptions Underlying the GMS Factor Shocks Are Overly Punitive and Don’t Meet a ‘Severe but Plausible’ Standard

SIFMA remains concerned that the CCAR approach to the trading book exposures unduly punishes capital market products and participants. As noted, one concern is that the Federal Reserve generates trading book and counterparty credit losses for the CCAR analysis through both the GMS and LCD components and the application of the macroeconomic scenario to trading book exposures in the severely adverse scenario.

There are also several embedded assumptions in the construction and sizing of the GMS factor shock which we believe are excessively harsh largely because the Fed describes the stress test standard as ‘severe but plausible.’ This is an underappreciated concept because post-stress test capital is not the only approach to sizing capital for banking organizations. There are several capital requirements in place to protect the resilience of large banking organizations during periods of market or economic uncertainly. As we discussed in our recent blog, requiring additional capital above-and-beyond our current rigorous capital framework, particularly when it is unanticipated and fairly speculative, will have real implications on the ability of a bank to inject capital and liquidity into economy. A recent BPI blog post noted the overly conservative approach of CCAR, and the very real potential the Fed may apply a COVID-19 adjustment.

SIFMA published a white paper last fall that analyzed and explained several concerns related to the GMS and LCD. These include:

- The implied severity of many of the individual GMS factor shock are extreme, low-probability events when compared to historical observations and empirical estimations.

As noted in the discussion of GMS factor shocks, there are several GMS factor shocks used in 2020 that are in excess of any historical one-day most adverse event. Moreover, there are several GMS factor shocks which are in excess of a series of daily price moves including over 10-day, 90-day or 180-day periods.

- The correlation assumptions underlying the GMS factor shocks are not empirically or historically supported and do not meet the FRB’s “severe but plausible” standard.

When the GMS shocks are observed as a portfolio of price movements, the Fed generally assumes all markets are positively correlated. This means that the assumptions underlying the GMS is that all markets will demonstrate severely negative price movements at exactly the very same time. It is true that the degree of correlation between asset classes may change over time or in a crisis, however, it is highly implausible to assume all markets will experience tail or near-tail events at exactly the same time.

- GMS assumptions regarding the duration of market dislocation for certain asset classes are not supported by empirical analysis or historical observation.

The Fed generally calibrates GMS factor shocks to represent a series of price movements over multiple days/months depending on the GMS factor shock and asset class. This would imply that a firm has no ability to sell or hedge a position which is not historically supported many all asset classes. For example, the discussion regarding B rated corporate credit spread shocks noted that the 2020 GMS factor shock was greater than the most adverse series of daily price moves equal to 6 months. Sizing the GMS factor shock in that way hypothetically assumes that the position cannot be reduced, sold or hedged. Generally, the more adverse the shock is in comparison to the most adverse price movement, the more punitive the implied holding period. Holding periods that are that punitive, add unnecessary severity into the GMS but also the LCD.

Concluding Thoughts

Clearly the 2020 GMS price shocks are significantly conservative in terms of historical adverse moves, and importantly, in comparision to the COVID-19 experience. Given the double tax on trading book and counterparty exposures driven by the application of the GMS and LCD and the application of the macroeconomic scenario under the severely adverse scenario is so harsh, there is no justification to layer an additional COVID-19 adjustement to capital markets products particularly when sizing the Stress Capital Buffer. Layering on an extreme tail scenario for capital market products on top of the already conservative 2020 CCAR framework will result in an unjustified increase in the SCB. This is particularly concerning when economic recovery is reliant on banks to provide credit and liquidity to households and businesses to facilitate economic recovery, contribute to orderly markets, and support financial intermediation in the capital markets.

Coryann Stefansson is Managing Director and Head of Prudential Capital & Liquidity Policy.

Credits:

- Katie Kolchin, CFA

- Ali Mostafa

- Bradley Harper

Appendix

The sections below highlight the findings and recommendations that were noted in our 2019 Study of the GMS and LCD

Section 1: Global Market Shock

| Key Findings | Recommendations |

| · The severity of any single GMS factor shock is an extreme, low-probability event when compared to historical observations and empirical estimations. | · Recommendation 1: GMS factor shocks should be tailored to reflect the liquidity and price stability characteristics of particular asset classes. |

| · The correlation assumptions underlying the GMS factor shocks are not empirically or historically supported, and do not meet the FRB’s “severe but plausible” standard. | · Recommendation 2: Correlation assumptions need to be rationalized and validated based on empirical analysis and historical observation in order to meet the “severe but plausible” standard. |

| · The extent of volatility in prior GMS shocks – in terms of severity and direction – conflicts with the FRB’s embedded assumption of near-perfect correlation and hinders capital planning. | · Recommendation 3: Year-over-year changes in stress testing should explore salient emerging risks and avoid unexpected, extreme or random swings do not facilitate capital risk identification and management. |

| · GMS assumptions regarding the duration of market dislocation for certain asset classes are not supported by empirical analysis or historical observation, conflict with other U.S. and Basel Committee on Banking Supervision (BCBS) standards (e.g., the LCR and the Fundamental Review of the Trading Book) and do not pass a “severe but plausible” test. | · Recommendation 4: Replace the blunt three- to six-month GMS with a framework that accounts for the liquidity and price stability of assets. Assets with high price stability and liquidity should be calibrated towards historical observation, at a maximum of 30 days or fewer. |

Section 2: Large Counterparty Default (LCD)

| Key Findings | Recommendations |

| · The use of GMS shocks to estimate LCD losses leads to an overstatement of risk, particularly for the most liquid and easiest-to-hedge exposures.

· As recognized in multiple U.S. regulatory frameworks, the typical closeout period for counterparty default exposures is far shorter than the multi-month timeframe implicit in the GMS. · Other jurisdictions have evolved their LCD components to more closely mirror risks, counterparty vulnerability and market behaviors. | · Recommendation 5: Review and justify the LCD component to improve risk sensitivity and more closely mirror market practice.

· Recommendation 6: At a minimum, estimate LCD losses on the basis of extreme-but-plausible price moves over conservatively defined closeout periods, either by basing the LCD on a new set of price shocks defined independently of the GMS, or by applying scalars that adjust the GMS shocks down to closeout periods appropriate for counterparty default exposures. |

| · The FRB’s supervisory approaches to recovery rate modeling, including its assumptions, data and calibration, are not transparent. Specifically, the recovery rates that are employed in the annual test are not disclosed. This contrasts to the increased transparency of loss estimation models and annual loss rates. | · Recommendation 7: Increase the transparency and disclosure regarding recovery rate modeling, assumptions and data including empirical support. Recovery rates used in CCAR should be disclosed annually. |

Section 3: CCAR Framework and Approach

| Key Findings | Recommendations |

| · The FRB does not provide disclosure regarding how the GMS shocks are sized, including how calibration and correlation are considered, other than they are based on a “principle of conservatism” and a “severe but plausible” standard.

· The opacity in how the GMS shocks are constructed impedes the FRB’s ability to analyze and learn from these tests, and to improve upon its current supervisory approach. · The process surrounding the GMS and LCD components and their administration lacks the structure, transparency and consistency that exists in other parts of CCAR. | · Recommendation 8: Apply similar transparency to the determination of GMS shocks as is currently applied to the FRB’s macroeconomic scenarios. Additionally, employ controls or “guardrails” on GMS factor severity, correlation, volatility and calibration similar to what the FRB implemented with respect to House Price Index (HPI) and unemployment. Moreover, apply the same process type controls to the administration and communication of the GMS and LCD components’ annual process. |

| · The requirement to employ both GMS and PPNR modelling results in overestimation of losses and underestimation of available capital through double counting of losses and the instructions for calculation of pro forma capital.

· The GMS captures some assets that do not demonstrate the characteristics of more traditional trading exposures. Given the underlying objectives of the GMS, the impact on some asset classes is inappropriate and may over or understate losses. | · Recommendation 9: Revise the GMS and LCD components and PPNR framework to eliminate the double counting issue either by a developing a transparent supervisory workaround, or by zeroing out the GMS and LCD components results in the first quarter of the PPNR. Simultaneously, address the underestimation of available capital by implementing a max loss cap (losses and deductions) to avoid capital requirements that could exceed the current value of securities and investments, and allow firms to calculate deductions in post-stress loss capital ratios using post-stress loss asset values.

· Recommendation 10: Omit non trading-centric asset types from the GMS, as is currently the case with the carve-out of fair value non-trading loans. These assets would remain subject to PPNR modelling. |

[1] Ally Financial Inc, American Express Company, Bank of America Corporation, The Bank of New York Mellon , Barclays US LLC, BMO Financial Corporation, BNP Paribas USA, Inc., Capital One Financial Corporation , Citigroup Inc., Citizens Financial Group, Inc., Credit Suisse Holdings (USA), DB USA Corporation , Discover Financial Services DWS , Fifth Third Bancorp, The Goldman Sachs Group, Inc., HSBC North America Holdings Inc., Huntington Bancshares Incorporated, JPMorgan Chase & Co., KeyCorp, M&T Bank Corporation, Morgan Stanley, MUFG Americas Holdings Corporation, Northern Trust Corporation, The PNC Financial Services Group, Inc, RBC USA Holdco Corporation , Regions Financial Corporation, Santander Holdings USA, Inc., State Street Corporation, TD Group US Holdings LLC, Truist, UBS Americas Holdings LLC, U.S. Bancorp, Wells Fargo & Company.

[2] Any firm that is subject to supervisory stress tests and that has aggregate trading assets and liabilities of $50 billion or more, or aggregate trading assets and liabilities equal to 10 percent or more of total consolidated assets, and is not a large and noncomplex firm.

[3] Firm’s subject to the GMS and LCD include Bank OF America Corporation, Barclays US LLC, Citigroup Inc., Credit Suisse Holdings (USA), DB USA Corporation, The Goldman Sachs Group, Inc., HSBC North America Holdings Inc, JP Morgan Chase & Co, Morgan Stanley, UBS Americas Holdings LLC and Wells Fargo & Company.

[4] BHCs only subject to the LCD include The Bank of New York Mellon and State Street Corporation.