The Federal Reserve Should Remove “Gold-Plating” in the Basel III Endgame

- Dr. Guowei Zhang, Dr. Peter Ryan and Carter McDowell

To Ensure International Comparability and Enhanced Financial Stability: Part IX in Our Series on US Bank Capital Requirements

- The post-Global Financial Crisis capital rules applicable to the largest U.S. banks are already super-equivalent (i.e., “gold-plated”) to the internationally agreed Basel standards and the proposed (or finalized) rules in most other major jurisdictions.

- The Federal Reserve’s proposal implementing the Basel 3 Endgame in the United States contains a suite of both technical and structural changes to the Basel standards that constitute additional U.S. gold-plating. The continued U.S. gold-plating drives the large, expected increase in capital requirements for large U.S. banks’ capital markets activities.

- As a result, the U.S. proposal undermines the stated objectives of the Basel 3 reforms, which were in large part to promote cross-bank and cross-jurisdictional comparability of risk-based capital requirements.

- Excessive capital requirements would (1) constrain banks’ capacity to provide credit and support the capital markets and the broader economy; (2) accelerate the shift of financing activities outside of the banking system; and (3) further diminish liquidity in key markets and exacerbate financial stability risks. Thus, the Federal Reserve and the other banking agencies should remove the U.S. gold-plating in the U.S. proposal and certain other elements of the U.S. capital framework to ensure cross-jurisdictional comparability and enhance financial stability.

Background

All major jurisdictions including the EU, the UK, and the United States have published their proposals to implement the Basel 3 Endgame (“B3E”) or have finalized their implementation. In July 2023, the U.S. banking agencies released their proposal implementing the B3E in the U.S. (“U.S. proposal”). The U.S. proposal contains a suite of changes to the Basel standards that constitutes a further U.S. gold-plating of the Basel international standards beyond the existing super-equivalence that is built into the current U.S. capital rules. This decision to gold-plate the international standards in the U.S. proposal contradicts the stated objectives of the Basel 3 reforms, which were designed to promote cross-institutional and cross-jurisdictional comparability of risk-based capital requirements.

This blog identifies areas in which the U.S. proposal gold-plates the international standards and benchmarks the U.S. proposal with the Basel standards, the EU implementation, and the UK proposal to highlight areas of U.S. divergence. As discussed below, the U.S. banking agencies should remove these gold-plated features to ensure international comparability and enhance financial stability.

Where does the US proposal gold-plate the internationally agreed Basel standards?

Table A1 of the Appendix presents a non-exhaustive list of areas in which the U.S. proposal gold-plates the Basel 3 standards. And some policy decisions in the EU and the UK implementation. At a high level, the gold-plating in the U.S. proposal can be classified into two broad groups – technical and structural.

Some of the technical gold-plating in the U.S. proposal include:

1. Adopt the SFT haircut floor framework with indications of materially broadening its scope and stringency. The Basel 3 standards include minimum haircuts on non-centrally cleared securities financing transactions (“SFT haircut floor”), which were devised by the Financial Stability Board (“FSB”) to “limit the possible build-up of leverage outside the banking system and reduce the procyclicality of that leverage.”[1] The SFT haircut floor requires banks to receive a minimum amount of over-collateralization on certain SFTs with counterparties that are not subject to prudential regulation.

The European Banking Authority’s 2019 Report analyzed carefully the SFT haircut floor framework and recommended against implementing it in the European Union at this time due to the fact that it “could theoretically lead to a more risky situation for institutions than the status quo … while at the same time it would be unclear whether the application of the framework will have a positive effect in practice on limiting the build-up of leverage outside the banking system.” Many other major jurisdictions, e.g., the UK and Canada, have reached similar conclusions, and thus have decided not to adopt the framework as part of the Basel 3 Endgame implementation. However, the U.S. proposal not only implements the SFT haircut floor but gives clear indications that the agencies are considering broadening the scope of the framework and its stringency. This potentially broadened scope/stringency would include covering more counterparties (e.g., prudentially regulated financial institutions)[2], more security types (e.g., U.S. Treasury securities)[3], and setting higher haircut floors[4]. The proposal offers no evidence, nor justification, to warrant the need for this broader scope and higher stringency.

2. Floor internal loss multiplier (“ILM”) at 1. The ILM of the Basel’s new standardized measurement approach (“SMA”) for operational risk was designed to reflect banks’ operational risk losses history in the resulting capital requirements. For banks that have strong operational risk management practices and thus minimal historical operational risk losses, the ILM can go below 1. Otherwise, the ILM will be greater than 1. The U.S. proposal floors ILM at 1, i.e., regardless of the strength of banks’ operational risk management practices. The proposed floor will result in higher operational risk capital requirements and create perverse incentives contrary to prudent risk management practices. Additionally, as discussed later the Basel SMA (without flooring ILM at 1) produces capital requirements that are well in excess of banks’ historical annual operational risk losses.

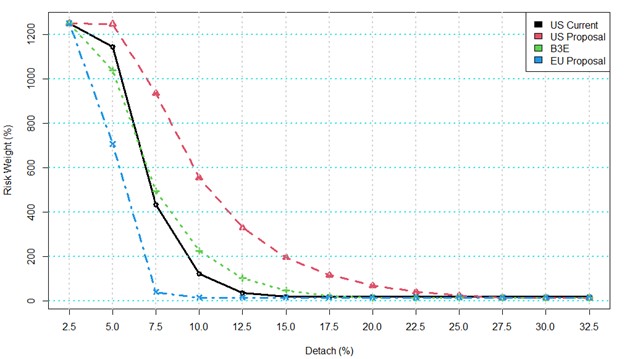

3. Raise residential mortgage risk weight by 2000 basis points above the Basel standards. The U.S. proposal assigns to residential mortgage exposures a risk weight that is 2000 basis points above the Basel standards. The Urban Institute examined the historical U.S. residential mortgage loss experiences and concluded that “[t]here is no logical argument for the bank capital requirements proposed in the [U.S. proposal].”[5] Gold-plating risk weight for residential mortgage exposures and the doubling of “p factor”[6] (i.e., from p=0.5 in the current U.S. capital rules to p=1 in the U.S. proposal) in the securitization risk weight function directly translate into materially higher costs for large U.S. banks’ holdings, as well as trading, of mortgage-backed securitization exposures, as shown in Figure 1 below. Capital requirements under the U.S. proposal for holdings of mortgage-backed securitization exposures are expected to range between 0.75x-9.80x current U.S. capital levels.[7]

UK Prudential Regulatory Authority’s (“PRA”) Basel 3.1 proposal “set[s] a p-factor of 0.5 for exposures to STS securitisation and a p-factor of 1 for exposures to non-STS securitisations”.[8] Concerned with the “[risk-weighted amount] resulting from the application of the SEC-SA is not commensurate with the risks posed to the institution or to financial stability”, on October 31, 2023, PRA published a discussion paper offering 3 options for “adjustments to the Pillar 1 framework for determining capital requirements for securitisation exposures”.[9]

Figure 1. Risk Weight of Mortgage-Backed Securitization Exposures under the Current U.S. Capital Rules, the International B3E Standards, the U.S. Proposal, and the EU Proposal.

4. Include centrally cleared derivatives in Credit Valuation Adjustment (“CVA”) capital requirements. Post the Global Financial Crisis, the G20 agreed that “all standardised [derivatives] contracts should be cleared through central counterparties (“CCPs”).”[10] To incentivize central clearing, the Basel standards exempt from CVA capital requirements centrally cleared derivatives.[11] The U.S. proposal adopts part of the exemption for minimum CVA capital requirements, i.e., exempting derivatives transacted directly or indirectly through a clearing member with a qualified central counterparty (“QCCP”). However, the client-facing leg of the client-cleared derivatives transactions would be considered OTC transactions for the purpose of the U.S. capital rules and are subject to minimum CVA capital requirements. The U.S. GSIB surcharge proposal includes the client-facing leg of the client-cleared derivatives transactions into the GSIB score calculation leading to a higher surcharge. Additionally, large U.S. banks would be required to calculate CVA losses arising from all derivatives transactions, including centrally cleared derivatives, and reflect it in the Federal Reserve’s Stress Capital Buffer (“SCB”) trading and counterparty loss estimates – effectively reversing the exemption included in the Basel standards.[12]

Some of the structural U. S. gold-plating in the U.S. proposal include:

1. Tie supervisory stress tests to capital requirements. The Federal Reserve’s SCB (which is floored at 2.5%) replaced the Capital Conservation Buffer (“CCB”, which is fixed at 2.5%) in the Basel standards. The SCB ties the results of the annual supervisory stress test to large banks’ mandatory capital requirements.[13] The supervisory stress test captures both trading and counterparty losses (via the Global Market Shock component or “GMS”) and operational risk event losses in a highly conservative manner. In particular, the GMS loss is estimated assuming severe losses within each asset class and no diversification across asset classes. Consequently, the stress losses estimate is more conservative than empirically “plausible”.[14]

The U.S. proposal’s market risk and CVA risk frameworks capitalize trading and counterparty losses in a manner that largely mirrors the GMS.[15] The proposal’s SMA framework capitalizes operational risk more than adequately. In fact, the SMA (without flooring ILM at 1) produces capital requirements that are about 14x banks’ historical annual operational risk losses[16], and “about double the maximum amount of loss ever experienced”[17] Consequently, the U.S. proposal plus the SCB would result in capital requirements that are excessive and incommensurate with large banks’ trading, counterparty and operational risks.

In contrast, both the European Central Bank (“ECB”) and UK PRA avoid “double accounting”, and thus over-capitalizing, these risks in setting their capital requirements. In particular, “[a]s a principle, the PRA would not double count capital requirements for the same risks in Pillar 1 and Pillar 2A.”[18] The ECB states that “individual add-ons might be adjusted to eliminate any possible double counting where the same risk drivers are addressed simultaneously under different risk categories.”[19] This is an approach that the Federal Reserve ought to follow.

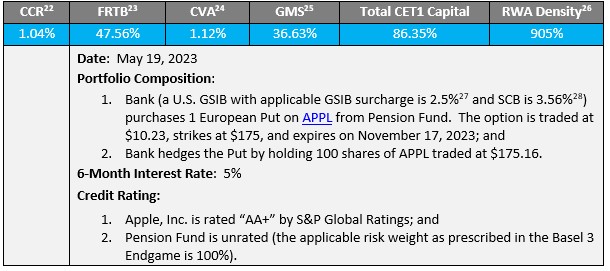

To illustrate the conservatism in capital requirements resulting from the combination of the U.S. proposal and the SCB, Table 1 below shows the capital requirements on a simple well-hedged equity portfolio – consisting of a vanilla put option on Apple stock hedged with cash equity. The aggregate capital requirements under the U.S. proposal and the GMS losses would amount to 86% of the market value of this portfolio. And the FRTB plus GMS losses account for 84% of the market value. The effective risk weight, i.e., RWA Density, of 905% suggests that the U.S. proposal capitalizes this portfolio on the basis that it is more than twice as risky as “speculative unlisted equity exposures” to which the proposal assigns a risk weight of 400%.[20]

This outcome does not even factor in the operational risk capital requirements attributed to trading this portfolio. The SMA is based on the weighted sum of three business indicators (“BI”). One of BI’s is the Financial Component – which capitalizes the net Profit/Loss on trading activities.[21] As a result, banks’ trading activities are separately capitalized through the SMA under the U.S. proposal. This leads to further overcapitalization of this simple portfolio.

Table 1. CET1 Capital Requirements as Percentage of The Portfolio’s Market Value.

2. Institute a more punitive GSIB surcharge methodology than the Basel standards. Along with the U.S. proposal, the Federal Reserve proposed amendments to the GSIB capital surcharge. However, the amendments would not alter the fundamental structure of the U.S. GSIB surcharge calculation. The Federal Reserve uses two methods – Method 1 and Method 2 – to calculate GSIB surcharges with the higher of the two calculations being the binding requirements. Method 1 is the approach in the Basel standards and in other major jurisdictions. Whereas, Method 2 was designed by the Federal Reserve and applies to U.S. GSIBs only. The Method 2 surcharge, in practice, is higher than that of Method 1. And increases automatically as the U.S. economy grows even without changes to a U.S. GSIB’s systemic risk profile.[29]

3. Eliminate the risk-sensitive modeled approaches. To reduce the excessive variability in risk-weighted assets, the Basel standards set stricter requirements for use of models and sets out an output floor for modeled risk-weighted assets using the regulators-set standardized approaches. The role of models is two-fold: it is used to calculate capital requirements and facilitate prudent internal risk measurement and management practices. Tying capital requirements to internal risk management incentivizes banks to measure and manage risks more accurately and appropriately. It also encourages responsible financial innovation. Standardized approaches, however, can not readily be used, if at all, for internal risk management. Though relatively simple and more conservative, they inevitably penalize certain exposures and reward others.

The U.S. proposal only allows models for general market risk and removes modeled approaches everywhere else including for issuer default risk, i.e., idiosyncratic market risk. The elimination of modeled approaches in the U.S. capital framework and almost exclusive reliance on regulator-set standardized approaches to set capital requirements contribute to the expected excessive increase in capital requirements. This risks homogenizing banks’ business models and exposures, thereby, exacerbating financial stability risk.

4. Require multiple sets of capital calculations even though many calculations are ex-ante largely compliance exercises. The Basel standards set out a two-stack capital framework – standardized approaches and modeled approaches. For the latter, the resulting risk-weighted assets amount cannot be lower than 72.5% of standardized approaches (“Output Floor”). The U.S. proposal, however, essentially sets out a tri-stack capital framework – U.S. standardized approaches (“Collins Floor”), output floor, and the expanded risk-based approach (“ERBA”, whereby modeled approaches for credit risk and idiosyncratic market risk are removed).

Under the U.S. proposal, the output floor becomes fully effective once the final rule comes into force. However, the Basel standards offer a 5-year phase-in period during which the floor starts at 50% and gradually rises to 72.5% at the end of the phase-in period. As demonstrated in a separate blog,[30] the ERBA stack would produce higher capital requirements than both the output floor and the Collins floor ex-ante. As a result, these two additional capital stacks would amount to a costly compliance exercise for large U.S. banks.

Why Should the Agencies Eliminate Gold-Plating Associated with the Basel 3 Endgame?

U.S. policymakers have widely acknowledged the success of current capital and related prudential regulations. For example, Federal Reserve Chair Jerome Powell noted in his statement accompanying the release of the U.S. proposal, “the development and implementation of the Dodd-Frank Act and the Basel III accords followed a deliberative and thoughtful process that evolved over a period of several years” and as a result, the “U.S. banking system is sound and resilient, with strong levels of capital and liquidity.”[31]

The B3E was designed to “reduce excessive variability of risk-weighted assets (RWAs)” and ensure RWAs “comparab[ility]” across banks and jurisdictions.[32] The Basel standards achieve these objectives by instituting more stringent criteria for modeled approaches and relying more on risk-sensitive standardized approaches. Materially increasing capital requirements is not one of the objectives. In fact, the Basel Committee’s September 2023 Report suggested that the B3E was expected to increase capital requirements for G-SIBs globally by just 2.9%. However, the U.S. proposal gold-plated requirements drive an expected 20% increase in overall capital requirements for the largest U.S. banks. Moreover, there is well over a 100% increase in capital requirements for capital markets activities – leading to capital requirements that are incommensurate with risks as shown in Table 2.[33]

If adopted as proposed, the U.S. proposal’s gold-plating risks exacerbating inconsistencies in global capital requirements and could accelerate the shift of financing activities outside of the U.S. banking system. For example, the 2022 FSOC Annual Report notes that nonbank mortgage lenders now manage over 55% of U.S. mortgages compared to just 11% in 2011, and nonbank mortgage originations have increased by 27% since 2017 and now account for 66% of all mortgage originations.[34] The FDIC Chairman Gruenberg recently noted that “[t]hese nonbank mortgage companies typically rely on short–term wholesale funding, operating with limited loss-absorbing capacity.”[35]

The largest banks play a critical intermediary role play in U.S. capital markets and the broader economy. These large, proposed increases in capital requirements, especially those related to capital markets activities, would constrain banks’ capacity to intermediate in the capital markets, diminish market liquidity and accelerate the migration of financing activities outside of the banking system. This could negatively affect U.S. and global financial stability, and translate into less access to funding, higher costs and reduced availability of hedging/insurance products/services for U.S. corporations. As a result, this would lead to higher costs for U.S. consumers and hurt the entire U.S. economy. Additionally, less liquidity and wider bid-ask spreads in equity and bond markets would hurt U.S. consumers’ long-term savings portfolios.

Conclusion

The U.S. proposal contains a suite of changes that would gold-plate the internationally agreed Basel standards and drive an expected large increase in the capital requirements for the largest U.S. banks, especially as it relates to their capital markets activities. This also goes against the Basel 3 Endgame’s stated objective of enhancing the comparability of risk-weighted assets across banks and jurisdictions. And the resulting capital requirements are incommensurate with the underlying risks they are designed to capture, creating perverse incentives and severely constraining large banks’ capacity to intermediate the U.S. capital markets and support the broader economy. To avoid these outcomes and reduce financial stability risks, as well as to promote international comparability, the Federal Reserve and the other U.S. banking agencies should remove these gold-plated elements of the U.S. proposal and the existing U.S. capital framework.

Appendix

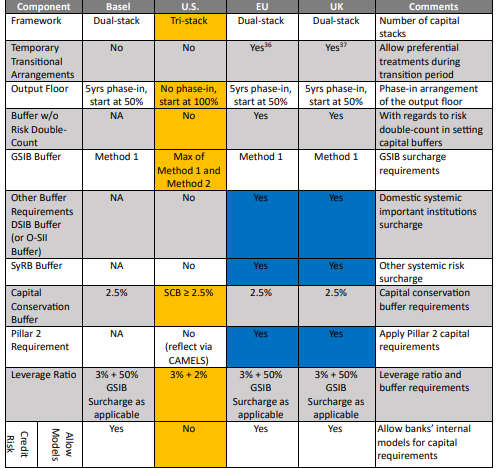

Table A1. A Non-Exhaustive List of U.S. Gold-Plating and A Cross-Jurisdictional Comparison (area highlighted in yellow indicates U.S. gold-platings, highlighted in blue indicates EU/UK gold-platings).

[1] https://www.fsb.org/wp-content/uploads/P070920-1.pdf

[2] See the U.S. proposal’s Question 54: What entities should be included or excluded from the scope of entities subject to the minimum haircut floors and why? For example, what would be the advantages and disadvantages of expanding the definition of entities that are scoped-in to include all counterparties, or all counterparties other than QCCPs? What impact would expanding the scope of entities subject to the minimum haircut floors have on banking organizations’ business models, competitiveness, or ability to intermediate in funding markets and in U.S. Treasury securities markets?

[3] See the U.S. proposal’s Question 55: What alternative definitions of “in-scope transactions” should the agencies consider? For example, what would be the pros and cons of an expanded definition of “in-scope transactions” to include all eligible margin loan or repo-style transactions in which a banking organization lends cash, including those involving sovereign exposures as collateral? How would the inclusion of sovereign exposures affect the market for those securities? What, if any, additional factors should the agencies consider concerning this alternative definition?

[4] See the U.S. proposal’s Question 58: What alternative minimum haircut floors should the agencies consider and why? What would be the advantages and disadvantages of setting the minimum haircuts at a higher level, such as at the proposed market price volatility haircuts used for recognition of collateral for eligible margin loans and repo-style transactions, or at levels between the proposed minimum haircut floors and the proposed market price volatility haircuts?

[5] https://www.urban.org/sites/default/files/2023-09/Bank%20Capital%20Notice%20of%20Proposed%20Rulemaking.pdf

[6] p-factor plays 3 roles in the securitization framework: (1) controls the degree of capital surcharge for securitization (i.e., the aggregate capital requirements for holding all tranches of a securitization exceed holding the underlying pool assets), (2) controls the allocation of capital requirements across different tranches of a securitization, and (3) smooths the cliff effects in capital requirements resulted from changes in capital requirements for the underlying pool assets.

[7] Risk weight applicable to super senior tranches is floored at 15% under the U.S. proposal vs 20% under the current capital rules, i.e., 0.75x.

[8] https://www.eba.europa.eu/regulation-and-policy/single-rulebook/interactive-single-rulebook/108627

[9] https://www.bankofengland.co.uk/prudential-regulation/publication/2023/october/securitisation-capital-requirements

[10] https://www.fsb.org/work-of-the-fsb/market-and-institutional-resilience/derivatives-markets-and-central-counterparties-2/

[11]https://www.bis.org/basel_framework/chapter/MAR/50.htm?tldate=20230222&inforce=20230101&published=20200708&export=pdf

[12] https://www.federalreserve.gov/apps/reportingforms/Report/Index/FR_Y-14Q

[13] Technically the SCB is a buffer. But because banks breaching it are required to limit, if not outright prohibit, capital distribution, banks generally treat the SCB as a minimum capital requirements.

[14] https://www.sifma.org/wp-content/uploads/2019/09/SIFMA-GMS-LCD-Study-FINAL.pdf

[15] https://www.sifma.org/resources/news/explaining-the-overlap-between-the-frtb-and-the-global-market-shock/

[16] https://orx.org/resource/basel-iii-and-standardised-approaches-to-capital-2023

[17] https://explore.pwc.com/baseliiiendgame-operational-risk/our-take-basel-analysis

[18] https://www.bankofengland.co.uk/prudential-regulation/publication/2022/november/implementation-of-the-basel-3-1-standards/interactions-with-the-pras-pillar-2-framework

[19] https://www.bankingsupervision.europa.eu/banking/srep/html/p2r_methodology.en.html

[20] https://www.bis.org/basel_framework/chapter/CRE/20.htm?inforce=20230101&published=20221208

[21] In particular, BI=ILDC+SC+FC. ILDC=min(abs(interest income – interest expense), 2.25%*interest earning assets)+dividend income; SC=max(other operating income, other operating expense)+max(fee income, fee expense); and FC=abs(net P&L trading book)+abs(net P&L banking book).

[22] The counterparty credit risk capital requirements are calculated according to 12 CFR Part 217 Subpart E §217.132.

[23] The market risk capital requirements are calculated using the FRTB SBM as prescribed in the Basel 3 Endgame MAR21 (applying the spot shock of 35% and volatility point shock of 77.78%) and FRTB DRC as in the Basel 3 Endgame MAR22 (setting cash equity maturity at 1-year).

[24] The CVA risk capital requirements are calculated using the BA-CVA as prescribed in the Basel 3 Endgame MAR50.

[25] The GMS losses are calculated using the spot shock of 26.3% and the volatility point shock of 26.5 as prescribed by the GMS of 2023 DFAST.

[26] The Basel 3 Endgame CRE20 assigns a risk weight of 400% to “speculative unlisted equity exposures”.

[27] The GSIB surcharge is the simple average of the surcharge applicable to the 8 U.S. GSIBs effective October 1, 2023. The simple average is 2.5%.

[28] The SCB is the simple average of the SCBs applicable to the 8 U.S. GSIBs effective October 1, 2023. The simple average is 3.56%.

[29] https://www.sifma.org/resources/news/the-federal-reserve-should-revise-the-us-gsib-surcharge-methodology-to-reflect-real-risks-and-support-the-economy/

[30] https://www.sifma.org/resources/news/understanding-the-proposed-changes-to-the-us-capital-framework/

[31] https://www.federalreserve.gov/newsevents/pressreleases/powell-statement-20230727.htm

[32] https://www.bis.org/bcbs/publ/d424.pdf

[33] As of year-end 2021, the aggregate market risk RWA for all large banks was $560 billion under the current U.S. standardized approach. The U.S. proposal estimates that “the increase in RWA associated with trading activity (market risk RWA, CVA risk RWA, and attributable operational risk RWA) would be around $880 billion for large holding companies”, which amounts to a capital increase of over 150%.

https://www.govinfo.gov/content/pkg/FR-2023-09-18/pdf/2023-19200.pdf

[34] https://www.consumerfinance.gov/data-research/hmda/summary-of-2021-data-on-mortgage-lending/#:~:text=The%20share%20of%20mortgages%20originated,from%2060.7%20percent%20in%202020.

[35] https://www.fdic.gov/news/speeches/2023/spsept2023.html#_ftnref25

[36] Transitional arrangements include (1) unrated corporates, (2) SA-CCR calibration, (3) residential real estate, and (4) output floor calibration. https://www.eba.europa.eu/sites/default/documents/files/document_library/Publications/Reports/2023/Basel%20III%20monitoring%20report/1062188/Annex%20to%20Basel%20III%20monitoring%20report%20as%20of%20December%202022%20-%20EU-specific%20Analysis.pdf

[37] Transitional arrangements include (1) equity exposures under both SA and IRB, (2) SA-CCR calibration, (3) CVA capital requirements, and (4) output floor calibration. https://www.bankofengland.co.uk/prudential-regulation/publication/2022/november/implementation-of-the-basel-3-1-standards

[38] Under the current U.S. capital rules, centrally cleared derivatives (i.e., CCP-facing) are exempt from minimum capital requirements for CVA risk, but client-facing leg of the client cleared derivatives are considered as OTC derivatives and subject to CVA capital requirements. Additionally, large U.S. banks are required to calculate CVA stress losses for purpose of the stress capital buffer requirement.