Top 10 Takeaways from SIFMA’s Economist Roundtable Mid-Year Survey

- Katie Kolchin, CFA, Managing Director, Head of Research

Listen to this post: Katie Kolchin, CFA, Managing Director and Head of SIFMA Research, highlights the top 10 takeaways from SIFMA’s 2023 mid-year economic survey. Then, hear from Dr. Lindsey Piegza, Ph.D., Chair of the SIFMA Economist Roundtable as she talks with SIFMA president and CEO Kenneth E. Bentsen, Jr. about the survey findings.

The Fed’s Policy Conundrum

In our semiannual economic surveys (published every June and December), we ask our Economist Roundtable to provide their assessment of the current economic environment and potential monetary policy actions. Last Wednesday, we published our 2023 mid-year survey.

Our Economist Roundtable estimated 2023 GDP growth at +0.5% (median forecast, 4Q/4Q), followed by +1.7% for 2024. 92.3% of economists expect a long-term potential GDP growth rate of 1.5-2.0%, with 100.0% stating this is unchanged over the last twelve months. The main factors impacting economic growth were identified as:

- For 2023: Inflation, tight labor market, regional bank turmoil/credit tightening, U.S. monetary policy

- For 2024: U.S. monetary policy, U.S. consumer spending, recession threat, tight labor market

Monetary policy. Fiscal spending. Economic reopening post-COVID. Supply chain disruptions. A war. That was already a lot for an economy to digest. Then we added on the regional bank turmoil and the debt ceiling debate (now resolved). It is no wonder the economy and inflation are where they stand today.

In this survey, we analyzed inflation – drivers and expectations for the path back down to the Fed’s 2% target – and the economy, in particular the labor market and the consumer, as well as recession expectations. The report also includes a pictorial view of the Fed’s monetary policy conundrum:

- Continue hiking?

- Pause to assess the monetary policy lag and other factors (ex: credit tightening)?

- When to begin the pivot (rate cuts)?

The Fed has repeatedly stated that it will be data-dependent. Unfortunately, the tone of the data is continuously changing and can even send opposing signals on the same day (see the May jobs report). With data all over the map, so must be the Fed when analyzing its next move.

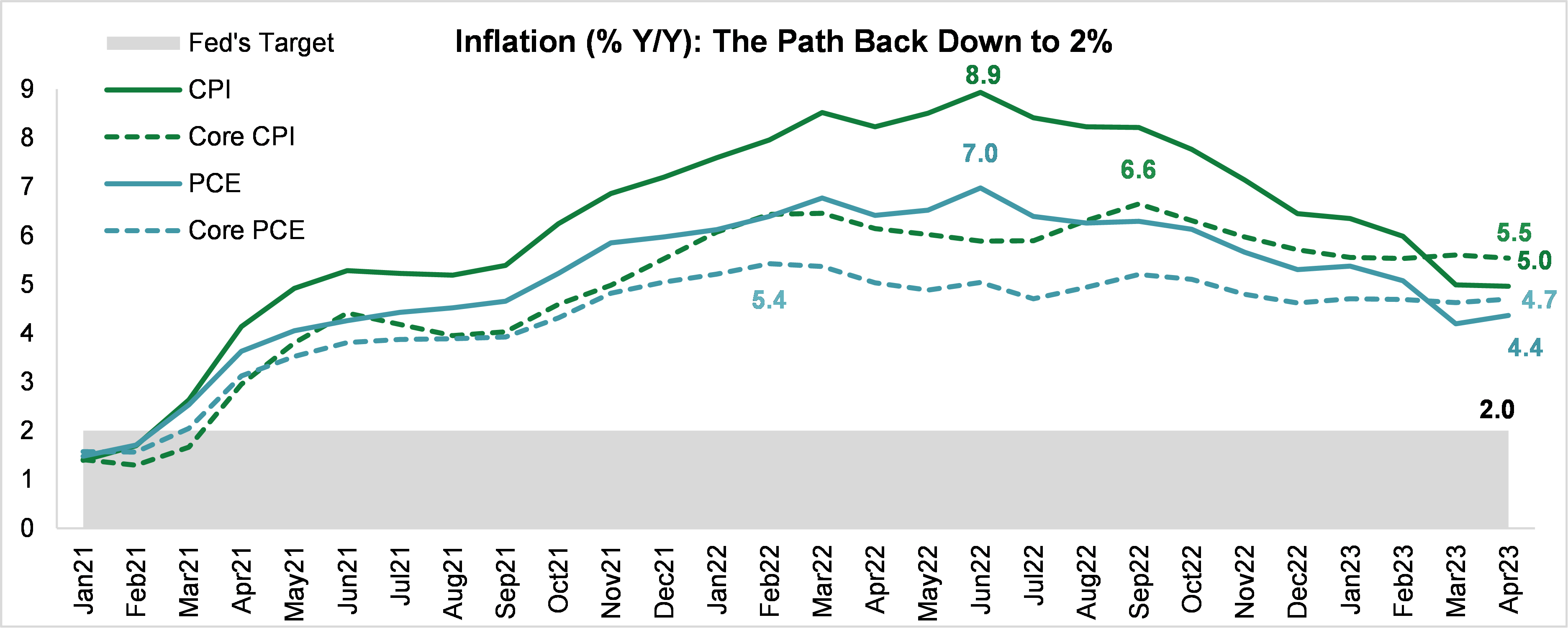

First, we highlight where we are with inflation metrics (Y/Y change, as of April) and how this compares to peak levels and the path back down to the Fed’s target of around 2%:

- Consumer Price Index (CPI) +5.0%; peak +8.9% in June 2022, 3.0 pps above target

- Core CPI +5.5%; peak +6.6% in September 2022, 3.5 pps above target

- Personal Consumption Expenditures (PCE) +4.4% – the preferred metric used by the Fed to set monetary policy – peak +7.0% in June 2022, 2.4 pps above target

- Core PCE +4.7%; peak +5.4% in February and March 2022, 2.7 pps above target

Source: FRED, SIFMA estimates

Next, we highlight the top ten survey results from our Economist Roundtable:

The Economy: Inflation, Labor Market, & Recession

#1. 83.3% of respondents believe price pressures on the way back down – PCE estimated to end 2023 at +3.8% Y/Y and end 2024 at +2.6% (+4.4% as of April) – but disinflation momentum will slow, with 50.0% responding inflation will not reach the Fed’s preferred 2% target until 2H24 (50.0% of respondents believe the Fed would tolerate a 2.0-2.5% range).

#2. Economists ranked the components impacting the aggregate inflation rate in order: (1) demand side, (2) the labor component, and (3) supply side. The factors listed as most important to core inflation forecasts include: consumer spending on services, stickiness of wage increases, historically hot labor market, and monetary policy.

#3. 81.8% of respondents believe we are not in a wage-price spiral. With wages +4.3% in May, versus +5.5% a year ago, 91.7% of respondents believe we have reached a peak in wage pressures. 70.0% of respondents expect growth to return to the historical +3.0% level (three-year pre-COVID average) by 2024.

#4. 50.0% of respondents believe the U3 unemployment rate needs to increase to 4.0-4.5% to meaningfully impact inflation, with 58.3% of respondents expecting to reach this U3 target rate by 2024.

#5. None of the respondents believe the U.S. is already in a recession, while 69.2% of respondents believe the U.S. will enter in a recession

Monetary Policy: Fed Rate Actions

#6. Our Economist Roundtable expects the peak Fed Funds rate to be 500-550 bps to be achieved by 2Q23, 78.6% of respondents each. We are already at this level.

#7. Monetary policy comes with a lag time before working its way into the economy. 38.5% of respondents believe the lag time is 9-12 months. As such, 92.3% of respondents think the Fed should pause and assess the impact of earlier rates hikes, with 91.7% of respondents believing this pause should take place in 2Q23.

#8. As to when the Fed will pivot and begin cutting rates, 71.4% responded 1Q24, with 76.9% of respondents believing it will take over 100 bps of cuts before stabilizing.

#9. 66.7% of respondents estimate the corresponding credit tightening post the regional bank turmoil is equivalent to 50 bps of additional Fed rate hikes – putting the implied Fed Funds rate at 5.50-5.75%, at or greater than the expected peak rate.

#10. As to whether this credit tightening should be a factor in the Fed’s decision-making for further rate actions: 91.7% of respondents noted that it should be and that it is/will be.

The full report can be found here.

Katie Kolchin, CFA, is a Managing Director and Head of SIFMA Research. She is also the author of SIFMA Insights.

—

Note: This survey was conducted between May 15-26, 2023.

The SIFMA Economist Roundtable brings together chief U.S. economists from over 20 global and regional financial institutions. SIFMA Research undergoes a semiannual U.S. Economic Survey with this group, analyzing the median economic forecasts of Roundtable members, published prior to the upcoming Federal Open Market Committee (FOMC) meetings in June and December. In those reports, we analyze the Economist Roundtable’s expectations for: GDP, unemployment, inflation, interest rates, etc. We also review expectations for policy moves at the upcoming FOMC meeting and discuss key macroeconomic topics and how these factors impact monetary policy.